“In the short run,

the market is a voting machine. In the long run, it is a weighing machine”

Said Warren Buffet.

However,

what he did not say was not quite how long the short run would last.

Given the froth in today’s market and how “concept stocks”

like Tesla, Netflix continue to scale new highs. In an artificially created world of euphoria

, (The Truman show as Seth Klarman

calls it), it is easy to get burnt by short positions.

Again, as someone who is endlessly interested in the

intersection of philosophy, physics and finance (read that as behavioural

economics), I find it extraordinary as to how the market for a long time

continues to “vote” for “talk” rather than the “walk” – viz., valuations

increase with announcements and introduction of concepts/prototypes, no matter

what the impact on cash flows)

- The market is ultra focussed on one metric that it tracks – all else, is irrelevant. For Amazon, it is revenue growth (no matter what the cost of the growth), for Netflix (it is the number of subscribers), for Tesla (the number of new cars)

- The CEO is a visionary and has had past success – there is a “halo” bias. Infact, a study that was run earlier showed that CEO’s who look good, talk glibly and can talk the language analysts want tend to push up stock prices higher (now, isn’t that obvious ?)

- The business model has operating leverage because :

- Network effect

- Creation of a strong brand

- Marginal costs of servicing are ostensibly low no matter how high the cost of acquisition (how many SaaS companies that burn money to acquire customers are eventually believed to become “cash flow” fountains once operating leverage kicks in)

- At one point, there is a serious threat of the company taking over the world. Think of all the "high fliers" at one time - Web van at one time threatened to wipe out all retailers, AOL was touted as the dark knight that would wipe out all media houses.

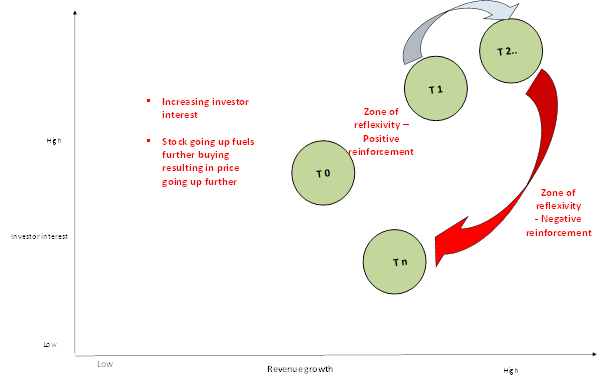

One of the bitter lessons that I learnt from my experience

of shorting “high momentum, high growth stocks“ is that they enter into what

George Soros calls the “zone of reflexivity”.

Where new actions reinforce the earlier actions resulting in the stock

price climbing higher and higher.

This results in one of the greatest paradoxes that you will

see in stock market history – fundamentals driven investors get burnt, get out

only to see the stock coming down finally.

Why does it happen?

While in the long run, a stock

price is determined by fundamentals, on a day to day basis it is determined by

the transient demand and supply. As long as there is someone (“the bigger

fool’s theory”) to pay higher for the same piece of paper, the price would

climb and vice versa.

The wisdom of crowds - "Crowds do not listen"

The trouble with that is that

investors have a huge herd mentality (much like the Great Beest migration) and

it is easy for a lion or a tiger to get crushed by the sheer momentum of the

beest. Modern day philosophy too

espouses the same thing (Charles

Mackay’s book – Extraordinary

popular delusions and madness of crowds)

|

| It's warmer and safer inside the herd ! |

"Men, it has been well said, think in herds; it will be seen that

they go mad in herds, while they only recover their senses slowly, and one by

one."

So what’s the solution ?

Is the momentum broken ?

No matter, how tempting it is, I

have learnt never to short a stock unless I am sure that momentum is broken. Ironically, the answer might lie with

technical analysis and a little bit of common sense.

External validation &

discountinuities

Look at what happened with the

recent Herbalife tug-of-war. Each point of discontinuity comes whenever there

has been a material event that has led to a loss of momentum. If FTC is

investigating herbalife, the stock falls 3-4%. If its has been cleared, it goes

up 3-4 %. Have the fundamentals changed ? Not in the least.As a corollary, I have found that

it is easier to short a stock which has far more externalities than one that

operates in a free market.

Cases in point :

- Regulatory interference : Herbalife – which operates in a regulated industry and comes under the purview of FTC and the business model comes under the laws of the land

- Quantitative externality: Allied capital/Lehman – financial services companies intrinsically have a lot many linkages that makes it easier for the market to sense triggers that can break momentum. For eg., increase in cost of funds (which happened when markets froze in Sep ’08), ability to validate the value of an investment from external sources (like David Einhorn did with the portfolio of allied capital).

- Fraud/misconduct: Even in case of shorts, often the most profitable ones have been fraud/misconduct. In most cases, frauds/misconducts are the lids that keep the “blackbox” of secrets closed (because frauds by their very nature are ones easy to establish). These often are the key points for reversal of momentum that allows for gravity to take over and allow a falling knife.

This gets compounded by the fact

that shorts are typically for a year and have to be rolled over frequently. In

a summary, it might actually be worth it to follow:

·

An activist investor (who can expose the flaw –

Einhorn in Allied/Lehman, Ackman in MBIA/Herbalife)

·

Wait for break of momentum (material event that

is bound to cause irreversible damage to the fundamentals – eg., adverse

preliminary findings from a FTC probe, margin calls/cost of funds going up for

a financial institution)

And then jump in to the short.

If ever there

were reasons to follow a "falling knife" (unlike the conventional worry about "catchign a falling knife"), a big short would be on.

In summary,

"Never ever short a stock just based on valuation. The market can stay irrational for longer than you can stay solvent. Remember to use the wisdom of crowds to your advantage."

No comments:

Post a Comment