One of the things that has fascinated me no end is how a high market share inevitably leads to a superior pricing power in the long run. I've used this as a fundamental thesis to identify and invest into companies that are leaders in a consolidated industry.

The reason why any marginal movement in marketshare (without any change to pricing yields or cost structures) is tremendously accretive to shareholders since it involves little or no incremental expenditure and hence all of the benefits accrue to the bottomline and hence to the shareholders.

This led me to discover one of the great truths in investing:

One of the biggest sources of shareholder value creation is a material movement of market shares (without any change in pricing yields/cost structures). Ironically, this runs counter to the popular intuition that it is new products/launches, it is actually new products/variants or improving sales/distribution/entry into new geographies that makes for the greatest impact.

The reasons are fairly intuitive - lower marginal costs, lower risk (of failure - since it is extending a proposition that is hopefully already well proven in the market).

Conversely, I have been quite amazed at the cost of becoming the lead consolidator in a fairly fragmented industry (think Amazon, even after all these years and with a cost structure that gives it an advantage over the brick and mortar retailers).

Being from India, I am amazed at the amount of money e-commerce retailers have to raise (and consequently burn through) to make a dent on what is ostensibly a large, growing market.

Even with a significant structure/cost advantage, lead consolidators in a fragmented market (where their product/service is not too differentiated from the rest) have an extremely hard time in expanding their bottomline and generate cash profitably.

This is a lesson that I drew on from Warren Buffet who compared small box retail as akin to running a marathon, competing with new sprinters at every turn. I fully understand the choices in front of, say a Jeff Bezos of Amazon, he can choose to raise prices now or penetrate further by improving market share. However, every time he gains some ground, he has to fight against a newer set of competitors.

Cases in point, have been the Future group in India, which has destroyed a lot of shareholder value, with bottomline and hence, sustainable value creation proving to be an elusive mirage and has seldom earned above its cost of capital.

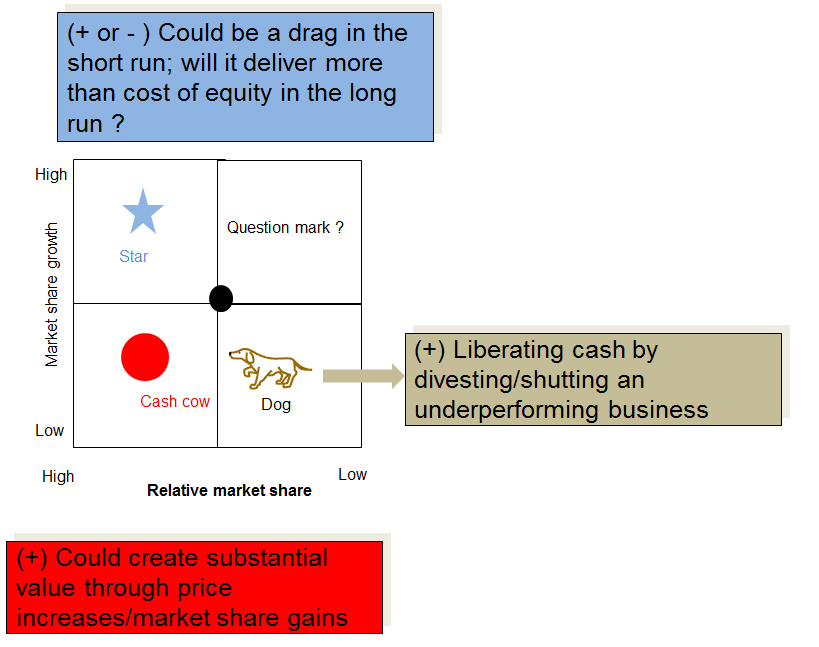

Too many times, the definition of a star or a dog or a question mark is'nt about the market share growth or the size, but about profitable growth. That's profit with a big P - the purists would argue that it is long term profits that need to be taken into consideration. For that, my answer is simple - long term cannot be more than 5 years; I have seldom seen traditional businesses that have continuously had losses in their core offering, who have scaled up profitably beyond.

To me, this question of allocating capital profitably represents a core strategic one - not an afterthought to a strategic one, like a lot of consultants believe. You do not decide about launching an iPhone in China, unless you understand its financial implications and if it will deliver above its cost of capital.

To me that represents the unison of strategy and capital allocation - a field that I am most passionate about. More to come in the later posts.

The reason why any marginal movement in marketshare (without any change to pricing yields or cost structures) is tremendously accretive to shareholders since it involves little or no incremental expenditure and hence all of the benefits accrue to the bottomline and hence to the shareholders.

This led me to discover one of the great truths in investing:

One of the biggest sources of shareholder value creation is a material movement of market shares (without any change in pricing yields/cost structures). Ironically, this runs counter to the popular intuition that it is new products/launches, it is actually new products/variants or improving sales/distribution/entry into new geographies that makes for the greatest impact.

The reasons are fairly intuitive - lower marginal costs, lower risk (of failure - since it is extending a proposition that is hopefully already well proven in the market).

Conversely, I have been quite amazed at the cost of becoming the lead consolidator in a fairly fragmented industry (think Amazon, even after all these years and with a cost structure that gives it an advantage over the brick and mortar retailers).

Being from India, I am amazed at the amount of money e-commerce retailers have to raise (and consequently burn through) to make a dent on what is ostensibly a large, growing market.

Even with a significant structure/cost advantage, lead consolidators in a fragmented market (where their product/service is not too differentiated from the rest) have an extremely hard time in expanding their bottomline and generate cash profitably.

This is a lesson that I drew on from Warren Buffet who compared small box retail as akin to running a marathon, competing with new sprinters at every turn. I fully understand the choices in front of, say a Jeff Bezos of Amazon, he can choose to raise prices now or penetrate further by improving market share. However, every time he gains some ground, he has to fight against a newer set of competitors.

Cases in point, have been the Future group in India, which has destroyed a lot of shareholder value, with bottomline and hence, sustainable value creation proving to be an elusive mirage and has seldom earned above its cost of capital.

Too many times, the definition of a star or a dog or a question mark is'nt about the market share growth or the size, but about profitable growth. That's profit with a big P - the purists would argue that it is long term profits that need to be taken into consideration. For that, my answer is simple - long term cannot be more than 5 years; I have seldom seen traditional businesses that have continuously had losses in their core offering, who have scaled up profitably beyond.

To me, this question of allocating capital profitably represents a core strategic one - not an afterthought to a strategic one, like a lot of consultants believe. You do not decide about launching an iPhone in China, unless you understand its financial implications and if it will deliver above its cost of capital.

To me that represents the unison of strategy and capital allocation - a field that I am most passionate about. More to come in the later posts.